This article is from ECHO Asia Note # 40.

[Editor’s Note: This article is a brief snapshot of the full-length publication, just recently published and made available. The full-length book can be found and downloaded free online at the Mekong Region Land Governance (MRLG) website, and we would encourage you to take advantage of this great resource. For further information, please contact the authors: micah.ingalls@cde.unibe.ch or jc.diepart@gmail.com]

The Mekong region lies at the intersection of Southeast, East and South Asia, between two Asian giants: China and India. It comprises five countries that host the bulk of the Mekong river watershed: Cambodia, Lao PDR, Myanmar, Thailand and Vietnam. The Mekong region is exceptional for its social and ecological richness. Home to 237 million people, the region includes 329 ethnic groups speaking 410 distinct languages, making the region one of the most ethnically-diverse in the world. The Mekong is also a global biodiversity hotspot, with a high degree of ecological and agricultural diversity.

The Mekong region has undergone rapid socio-economic growth over the past two decades alongside pronounced transformations in a number of key sectors. These changes have significantly altered relations between the rural majority and increasingly-affluent urban centres. Land—as both a foundation for national development and the livelihoods of millions of rural and agricultural communities—continues to play a central role in the Mekong region. In all five countries, smallholder farmers play a crucial role in the development of the agricultural sector and, through it, food security and economic growth. However, rural communities are being increasingly swept up into regional and global processes within which they are not always well-positioned to compete. Worse, they are often undermined by national policies that fail to ensure their rights or enable them to reap potential benefits.

Understanding the changing role and contribution of land to development is critical to inform policy, planning and practices toward a more sustainable future. The State of Land in the Mekong Region aims to contribute to a much-needed conversation between all stakeholders by bringing together data and information to identify and describe the key issues and processes revolving around land, serving as a basis for constructive dialogue and collaborative decision-making. The State of Land in the Mekong Region is structured around five domains: (1) the land-dependent people of the Mekong, including dynamics of rurality, agricultural employment and the on-going structural processes of demographic and agrarian transition; (2) the land resource base upon which this population depends, including land use and land cover, agricultural conditions and change, and the region’s natural capital; (3) the ways in which this land resource base is distributed across society, including smallholdings, large-scale land investments and other designations; (4) the security of land tenure, which depends on how land rights are recognized and formalized, and; (5) the conditions of governance and land administration that shape access to and control over land resources, including issues of transparency, equity, the rule-of-law and access to justice. The State of Land in the Mekong Region is framed by a number of key indicators within each domain and presents these on two levels. At the regional-level, it presents a comparative analysis of key indicators between the Mekong countries and an examination of transboundary process that shape and define land issues, including regional trade and investment flows in the land and agricultural sectors. At the country-level, data and information on key indicators are disaggregated and examined to identify country-specific conditions and trajectories of change.

The role that knowledge plays in the identification of key land issues and in structuring decisions and policies to address these is critical. Yet, information on land and natural resources is often lacking, inconsistent, contested and difficult to access. The State of Land thus provides a critical analysis of data and information—what is available in the public domain, what is not, and why these matter—with a view toward constructively identifying ways to improve the production, management and sharing of data and information.

Each country in the Mekong region is undergoing a structural transformation of its economy, generally moving away from agriculture as its dominant sector. While the agricultural sector continues to grow—in some cases impressively—its proportional share of Gross Domestic Product has declined due to the even-more rapid growth of their industrial and service sectors. This pattern varies significantly across countries, however. In Thailand and Vietnam, urbanization and industrialization are more advanced; the share of agriculture in GDP is lower and has been more or less constant over the last 25 years. In Cambodia, Laos and Myanmar, the share of agriculture in GDP is higher, but saw an important drop from 2010 to 2016 to 26.7, 19.5 and 25.5 percent, respectively.

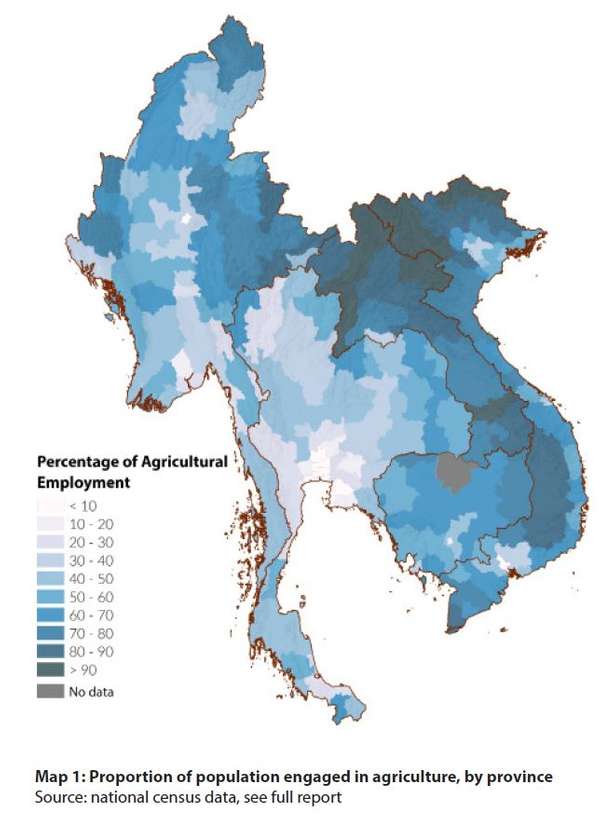

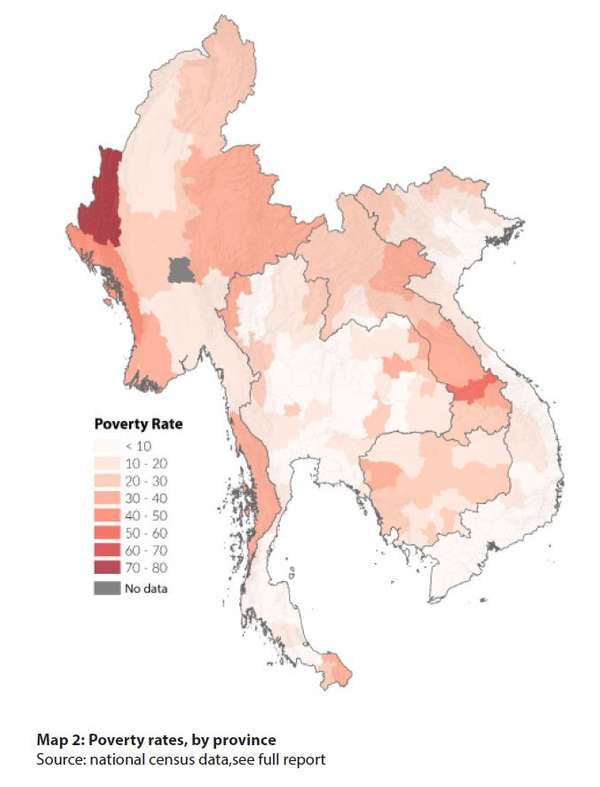

The proportion of the population engaged in agriculture has also declined, but at a much slower rate and still remains relatively-high (e.g. 80 percent in Laos and 70 percent in Vietnam, though 30 percent in Thailand) (Map 1). This and other evidence suggest that the agrarian transition—the transformation of agriculture under the forces of urbanization and industrialization—is an uneven process that is far from complete in the Mekong region. In Cambodia, Laos, Myanmar and Vietnam, the creation of jobs in the secondary and tertiary sectors lags significantly behind growth of the active labour force in rural areas, meaning that agriculture remains a strategic job provider for the vast majority of the rural population. Thus, access to land remains a central concern in the livelihoods of rural communities. This rural and agricultural population is also most likely to be poor. Poverty rates have been steadily declining across the Mekong, but this is much less true for rural areas (Map 2). Ninety percent of poor households in Cambodia, for example, are rural. In Thailand, the differentiation is perhaps more striking: while only one-third of households are considered rural, these comprise 80 percent of Thailand’s poor.

The incomplete character of the agrarian transition is increasingly visible in the demographics of the Mekong countries—in particular in the mobility of the rural population. Rural-to-urban migration flows are important, and related to urbanization and the opportunities afforded by growing industry and service sectors. However, these rural-to-urban migrations are dwarfed by the outsized flow of people from one rural place to another in search of land and economic opportunities, a dynamic typically under-recognized in the region. This rural-to-rural mobility has important implications for land distribution, access and tenure security. Cross-border migrations are both rising and typically associated with rural communities, as workers—especially the young—leave agricultural communities in Cambodia, Laos and Myanmar in search of employment, commonly in Thailand.

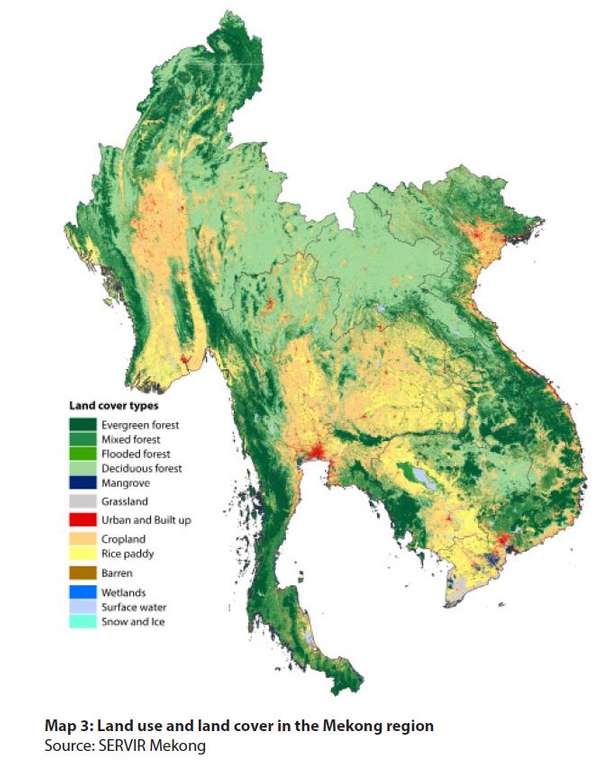

These economic and demographic transformations have been accompanied by dramatic changes in land use and land cover in the Mekong. At present, forests dominate the Mekong region (Map 3), comprising 47% of total land area (around 88.4 million hectares, ha) while agricultural land accounts for nearly 30% of land (or 54.4 million ha). This is rapidly

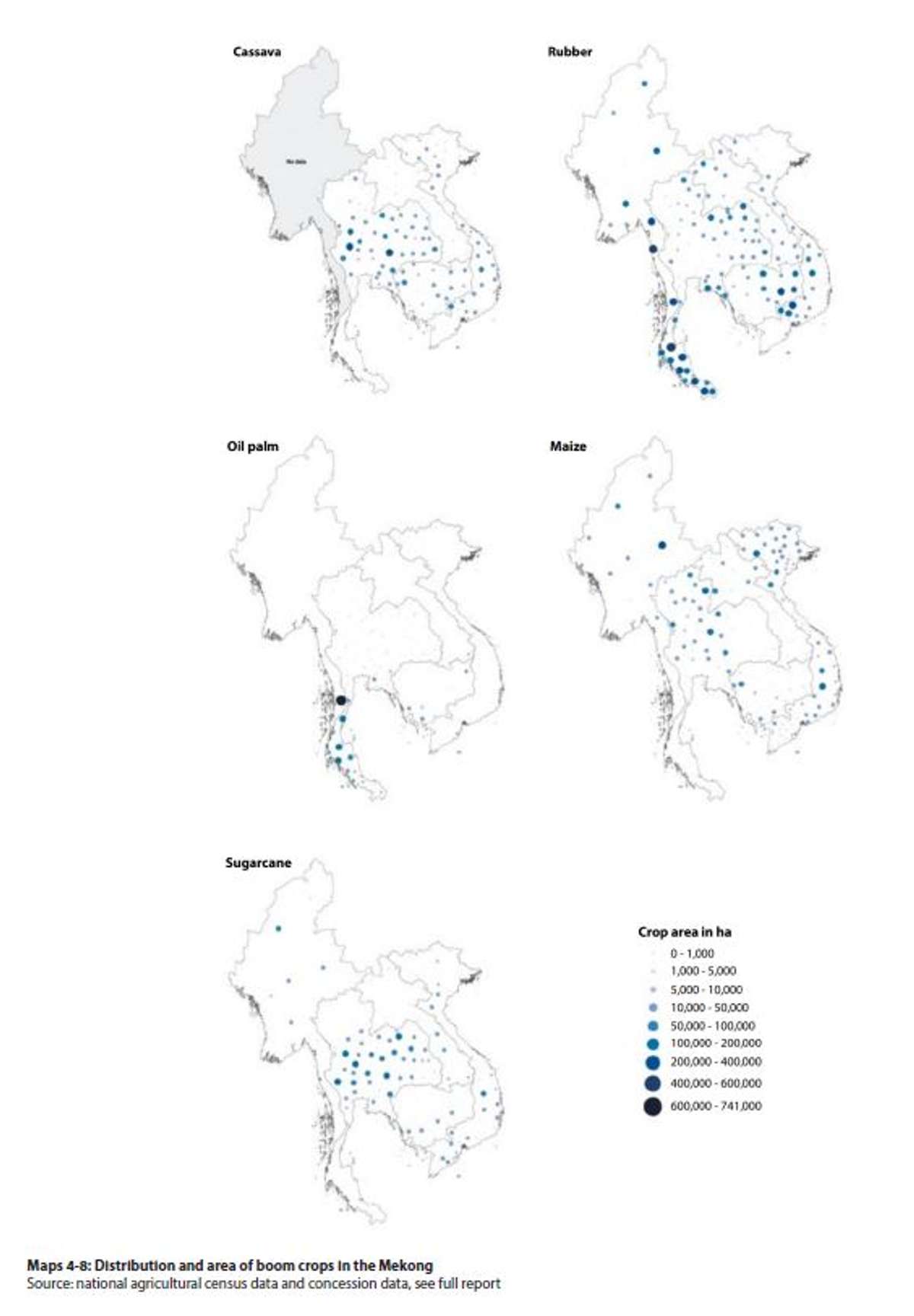

changing. Agricultural land across the region increased by more than 9 million hectares, or around 20 percent, between 1996 and 2015. At the same time, forest areas have declined, as non-forest uses (especially agriculture) encroach into remaining natural forests. These changes vary considerably by country. Vietnam has seen the most impressive expansion of agricultural land (around 65 percent), similar to patterns of agricultural expansion in (in descending order by proportion) Laos, Myanmar and Cambodia. Thailand, by contrast, experienced little change. Declining forest areas have been most pronounced in Cambodia and Myanmar, which have lost 22 and 21 percent of their forests, respectively. The expansion of agricultural land has also been accompanied by a number of changes in cropping patterns. The significant increase in the cultivated area of export-oriented commercial crops has resulted in a degree of diversity at the aggregate level, where cropping has partially shifted away from the overwhelming dominance of rice to include commodity crops. However, the replacement of natural vegetation and local, diversified cultivation systems has also brought about a profound degree of simplification: six crops alone—rice, cassava, maize, sugarcane, rubber and oil palm—now command fully 80% of all agricultural land in the Mekong. However, these crops are distributed unevenly (Maps 4-8).

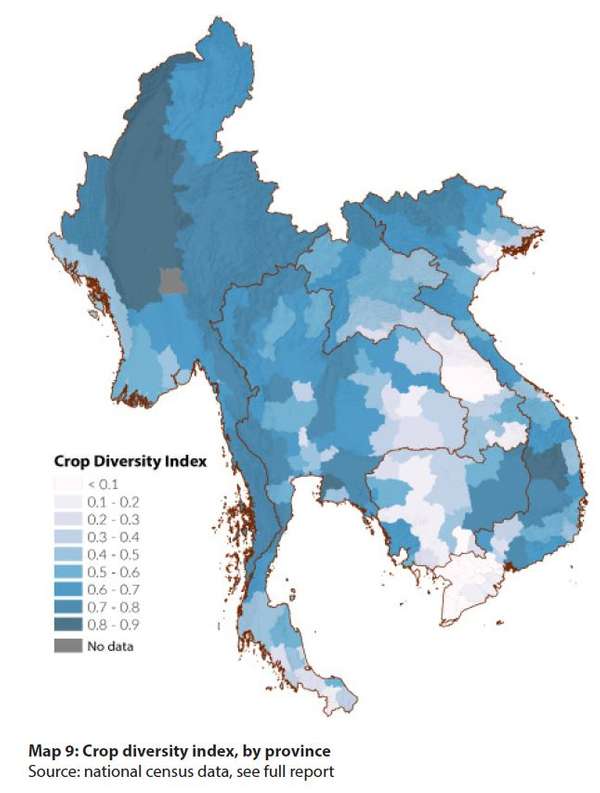

The crop diversity index (Map 9) provides a disaggregation of the diversity of cultivated species, proportional to their area of cultivation, at the subnational-level ranging from low diversity (near 0) to high diversity (near 1). The intensification of agricultural production is another pronounced trend and, while playing a major role in the growth of the agricultural sector, also has important implications for land degradation. Evidence suggests that the majority of the region’s land area shows medium- to high-levels of degradation, resulting from the loss of natural vegetation, mono-cropping, poor soil conservation technique and cultivation on fragile and easily-erodible soils in upland areas. The erosion of the natural capital base is a pressing concern with both immediate and long-term effects, particularly for those whose reliance on agriculture and forest resources—the poorest segment of society—is most direct.

The crop diversity index (Map 9) provides a disaggregation of the diversity of cultivated species, proportional to their area of cultivation, at the subnational-level ranging from low diversity (near 0) to high diversity (near 1). The intensification of agricultural production is another pronounced trend and, while playing a major role in the growth of the agricultural sector, also has important implications for land degradation. Evidence suggests that the majority of the region’s land area shows medium- to high-levels of degradation, resulting from the loss of natural vegetation, mono-cropping, poor soil conservation technique and cultivation on fragile and easily-erodible soils in upland areas. The erosion of the natural capital base is a pressing concern with both immediate and long-term effects, particularly for those whose reliance on agriculture and forest resources—the poorest segment of society—is most direct.

Agricultural land in the Mekong countries is primarily under the management of smallholder farmers, who thus remain the most important segment of the rural population with regard to the management of land, despite the increasingly-visible role played by agribusiness corporations and investor. However, agricultural land is unequally distributed among these smallholder farmers. The average landholding size per agricultural household varies widely between countries, from 0.7 ha in Vietnam to 3.1 ha in Thailand. Except in Laos, the average area of landholding per agricultural household has declined over the last 10 years. Variation in land holdings within each country is larger than variations between countries. The Gini Index of the distribution of smallholder agricultural land is relatively high (Cambodia: 0.47; Laos: 0.34; Myanmar: 0.48; Thailand: 0.49 and Viet Nam: 0.54) and has tended to increase in all five Mekong countries.

With the exception of Thailand, there has been a pronounced trend in all Mekong countries since the late-1990s toward an increasing number of large-scale land investments, as the governments of the Mekong countries have sought to leverage land deemed under-utilized to attract financial resources for development. The rationale is presented as self-evident: granting concessions in exchange for financial investment is necessary to turn untapped land into capital, boost the production of export commodities and stimulate opportunities for local development such as wage-labour, rural infrastructure, processing facilities and access to markets.Map 10 provides a disaggregation of the land Gini Indexes at the subnational-level. In these figures, landlessness is not adequately captured due to a lack of systematic data. Case studies indicate that the inclusion of landless households would demonstrate even higher disparities in land. Importantly, the inclusion of large- scale agricultural and forestry concession operated by companies shows that the distribution between all landholders is even more uneven (with Gini coefficients in Cambodia of: 0.64; Laos: 0.49; Myanmar: 0.53; Thailand: 0.49 and Viet Nam: 0.56).

Though some occurred earlier, large-scale land investments in the Mekong took off around 2006, and were further stimulated by the global financial crisis (2008), as rising food- and fuel-costs and risks associated with financial markets prompted global investors and agribusiness companies to invest in the Mekong’s emerging land market. Until 2011, the granting of land concessions was in full-swing (Figure 1). As a result, the agrarian structure of the Mekong countries has been considerably transformed. In total, 4.1 million hectares of land have now been granted to companies under various concession agreements in the agriculture and tree plantation sector alone. In Cambodia, Laos and Myanmar, land concession areas represent, respectively, equivalent to 37, 30 and 16 percent of the total area cultivated by smallholder farmers. Concessions of land in the mineral sector are substantial and, including exploration concession areas, significantly outsize agriculture and forestry concessions with at least 10 million ha. With the exception of Laos, a lack of available data limits detailed assessment.

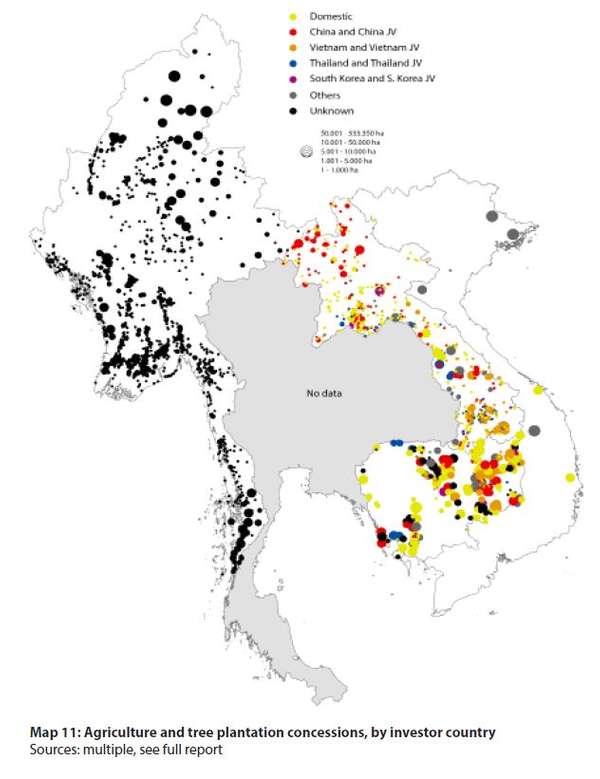

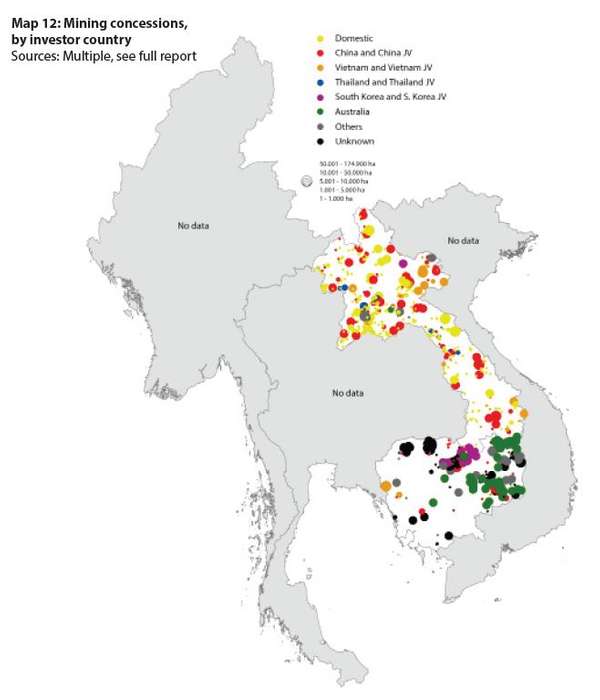

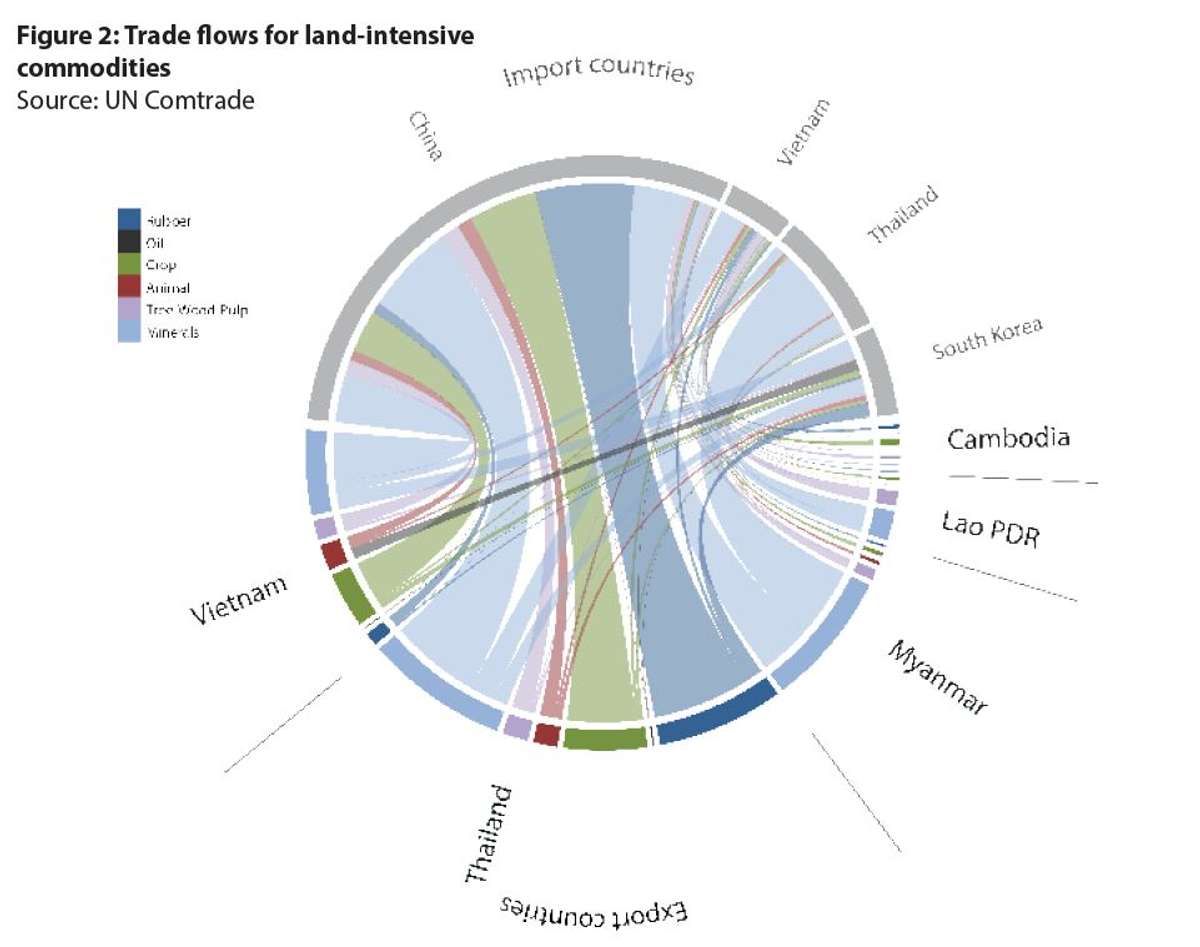

Most of the area under agricultural concession is devoted to the boom crops—rubber, sugarcane, oil palm, cassava and maize—that represent 76 percent of concession areas across the region. An important dimension of the concession landscape in the Mekong is the transboundary nature of investments and associated trade-flows between the Mekong countries themselves and their near-neighbours (Figure 2). While a significant amount of investment in land concessions is driven by domestic investors (43 percent in Cambodia and 31 percent in Laos), the second largest group are outward-going investors from China, Vietnam, Thailand and South Korea (together accounting for 36 percent of total concessions in Cambodia and 60 percent in Laos) (Maps 11 and 12).

Vietnam and Thailand function both as investors in large-scale land deals and importers, processors and exporters of the commodities associated with them. China is, by far, the largest end-market for regional exports of agricultural commodities (Figure 2).

In the main, the hoped-for benefits of these land investments have not been realized. While playing a role in rising GDP in host countries, state revenue has been less than anticipated and the social and environmental costs of these developments have generally exceeded their benefits. These costs have largely been borne by the rural poor. Fundamental to the problem has been an under-recognition of land tenure and local uses prior to acquisition. The dispossession of rural households from land concession areas accompanied by inadequate compensation— where such has been provided at all—has had a particularly negative impact, clearly at odds with the stated purposes of concession-based development strategies. The lack of return on these investments has prompted concerns among policy-makers across the region. In 2012, Laos and Cambodia both issued limited moratoria on new concessions. Processes of land conflict resolution have been activated but a particular point of concern in Cambodia, Laos and Myanmar revolves around the cancellation of concessions that are not performing or meeting their obligations. The underlying questions is whether these areas will be maintained as State land or be redistributed to farmers and communities. The tensions are clearly palpable and the future of concession-based development is uncertain.

The well-being of smallholders and their ability to gain benefits from their agricultural land depends to a large extent on the security of their tenure. Land titling and land use certificates are considered principal ways to provide formal legal recognition and to serve as collateral for loans. Land tenure formalization is most advanced in Vietnam, Thailand and Myanmar, though in the latter two of these countries titling tends to exclude large parts of the forest estate, a situation found also in Laos.

Beyond the titling of individual parcels, existing legislation and policies of the Mekong countries offer various forms of recognition of customary tenure.

Despite supportive legal frameworks, the practical formalization of customary tenure recognition has been slow, weak and irregular. The situation is particularly problematic in Myanmar where legislation has been generally regressive, providing no clear legal protection for customary tenure in, for example, shifting cultivation systems. Alternatively, a variety of co-management arrangements have been used across the Mekong as mechanisms to support traditional claims over land, forests and fisheries.

In response to structural changes in the land and agricultural sectors and the rapid changes in investment and commodity-flows brought about by the globalization of financial- and market-systems, the governance of land resources in the Mekong is undergoing a period of transformation previously unseen. The environmental and social impacts of large- scale land acquisitions and the rapid growth of land markets have triggered social unrest, raising concerns among policy makers resulting in—in some cases— policy responses such as moratoria (above), improved environmental and social impact assessment and compensation processes, and the prioritization of high-quality investments (those with relatively better social and environmental performance). Alongside these policy and regulatory changes, what has been most pronounced across all Mekong countries is the large gap between these and the practice of land administration. Corruption and a lack of public accountability remain key obstacles to addressing critical problems surrounding the land issue. The expropriation of land by the state for the promotion of investments has continued to struggle with the ambiguous nature of some specific land-deals—deals promoted for public purpose but often developed for private benefit. Closely related to these issues, the past decade especially has seen significant changes in civil society in the Mekong and the degree to which civil society organizations are able to effectively address land-related issues. These changes include both a degree of opening as well as a degree of closure, often in the same countries. In addition to a general lack of rights for civil society in some of the Mekong countries, of particular concern has been the recent clamping-down on such groups, often in response to political changes and uncertainties surrounding public corruption and land-related investments.

The rights of indigenous peoples and ethnic minorities to land and other resources vary widely across the Mekong. While national legislation in each country commonly includes provisions to ensure their rights, such provisions have generally not been sufficient to enable indigenous peoples and ethnic minorities to defend land claims or to protect traditional practices, such as shifting cultivation. Similarly, while the rights of women and female-headed households are typically enshrined in legal frameworks, there remains a need for significant improvements with regard to their protection in practice. A lack of gender-disaggregated data and information on tenure security for women is a key obstacle to consistent monitoring.

The Mekong is in the midst of substantial, far-reaching transformations with regard to land. The region is thus at a critical juncture wherein robust, inclusive and accountable decision-making are urgently needed. The continued dominance of regional and global financial- and commodity-markets suggests that the direction the Mekong countries take with regard to key land-related issues will be shaped in some measure by outside influences. The path forward depends on the degree to which these forces can be leveraged for the benefit of the rural and agricultural majority, rather than for the few. Whether the region is able to steer a course toward a more sustainable and inclusive future remains an open question, the answer to which will decide the future of the land and the people of the Mekong.

The State of Land in the Mekong Region is a production of the Centre for Development and Environment (CDE), University of Bern, and the Mekong Region Land Governance (MRLG) Project.

Citation for the full report:

Ingalls, M.L., Diepart, J.-C., Truong, N., Hayward, D., Neil, T., Phomphakdy, C., Bernhard, R., Fogarizzu, S., Epprecht, M., Nanhthavong, V., Vo, D.H., Nguyen, D., Nguyen, P.A., Saphangthong, T., Inthavong, C., Hett, C. and Tagliarino, N. 2018. State of Land in the Mekong Region. Centre for Development and Environment, University of Bern and Mekong Region Land Governance. Bern, Switzerland and Vientiane, Lao PDR, with Bern Open Publishing.

For further information, please contact: micah.ingalls@cde.unibe.ch or jc.diepart@gmail.com